Episode 6: Arvind Panagariya and Shruti Rajagopalan Talking Trade

7th February 2023

Arvind Panagariya and Shruti Rajagopalan Talking Trade

Episode 6: India's Trade Policy (1940-1965)

SHRUTI RAJAGOPALAN: Welcome to the discussion series on free trade and liberalization as part of the 1991 Project at the Mercatus Center. I’m Shruti Rajagopalan and in this conversation series I will be talking trade with professor Arvind Panagariya, who’s the director of the Deepak and Neera Raj Center on Indian Economic Policies and the Jagdish Bhagwati Professor of Indian Political Economy at Columbia University. In the past, he has served as the first vice chairman of NITI Aayog in the government of India and as the chief economist of the Asian Development Bank.

He is the author of a number of books, but for today’s conversation in particular, we will focus on his recent books, “Free Trade and Prosperity” and “India: The Emerging Giant.” Arvind, welcome back.

ARVIND PANAGARIYA: Thank you, Shruti. Glad to be with you.

RAJAGOPALAN: Taking off from our previous episode, Arvind, you told us in detail about the import licensing system. Can you walk us through what were the subsequent economic effects of this system, especially the long-lasting impact?

PANAGARIYA: Excellent, Shruti. This is a very good place to start.

Economic Impact of the Import Licensing System

PANAGARIYA: The licensing system undermined both the productivity at the firm and industry level, and the allocation of resources across industries. The effect was all around. Regarding the productivity at the firm and industry level, there were delays in obtaining imported machinery and inputs. It would take five to seven months for imports, one and a half years for capital goods, and so forth, so that clearly impacted productivity. There was unproductive use of resources. You had a big bureaucracy that had to be created to do the allocation. Entrepreneurs had to line up, wait outside the offices, wait for products to arrive and so forth. There were these delays, and unproductive use of resources themselves.

Then there was inflexibility, because of the unused capacity. If there are not enough imports that need to be imported but are not allowed to be imported then the excess capacity rises, investment goes unused. Then there were also rules of thumb used to make uniform allocations across firms and industries. You can imagine that that is going to create a lot of inefficiencies; some firms are more productive, others are less productive, some industries are more capable, others are less capable.

When you use these allocated rules, which are across the board, obviously, you are not allocating in the most efficient sort of way. There were also funny things that happened. Equipment would get imported, but if there are some components in the equipment, which have only a short life, like in the photography equipment, the bulbs that are required for photography, they have a limited life, they go off. Well, if you don’t have the bulbs, the entire equipment becomes unused. So, you have got that sort of problem. That’s one set of things that happened.

Then competition, of course, got impacted as well because import competition was automatically shut off if you are going to produce anything domestically. This was pretty much protection on demand provided, but domestic competition was also strangulated because if you can’t get foreign exchange for machinery, then competitors cannot enter the market. You kill that competition as well.

Finally, misallocation of resources because at a broad level, if you look at the full picture, obviously there was a huge anti-export bias created here. Both because a nominal exchange rate because the price levels domestically rose much more. Therefore, domestic market obviously becomes more lucrative than the foreign market, real exchange rate appreciates. All that created discrimination against exports as well.

Also, in terms of allocation, efficient and inefficient firms got treated pretty much equally. There was no way for more efficient firms to outdo the inefficient ones because they both get equal access to the imports. That clearly allows the inefficient firms to survive as well. These are various ways in which inefficiencies caught up, productivity is falling, resources being misallocated.

RAJAGOPALAN: Normally, people think that this kind of restrictive import licensing system only impacts imports and many of the economic effects that you talked about. But it also actually impacts exports and not just in a positive way, but adversely. Can you walk us through how India’s restrictive import licensing system actually also impacted India’s exports and, therefore, the export policy regime?

PANAGARIYA: Correct. This is all the joint impact of many interventions that we were doing. In a very simple sort of way, you see, what happens is that inevitably when you are restricting imports, that means that you do not need as much foreign exchange as you would if imports were open. What that does is it causes the domestic currency to appreciate. This reduces the value of the foreign currency, increases the value of the domestic currency. That’s one kind of mechanism through which this happens. Typically, import restrictions cause the domestic currency to appreciate in real terms.

Of course, an appreciated currency in real terms means that your returns to exports are low, and your returns to domestic sales are high. Automatically, products get channeled to the domestic sales, domestic market. This got reinforced, by the way, by a very fixed nominal exchange rate. This was a time when the international monetary system had adopted fixed exchange rates. For the developing countries, it would’ve been prudent.

For example, South Korea in the early 1960s, very quickly undertook very large devaluations of its currency, won. Because also South Korea didn’t have our kind of licensing, and the focus on heavy industries and so forth. There was internal flexibility as well. That devaluation really made the exports very lucrative. Very quickly, you see in the early ’60s, Korea’s light manufacturing exports take off in a very big way, and you see the composition of the export shifting away from agriculture toward these manufacturers.

In our system, we didn’t devalue, for one thing. We discussed earlier in the 1958 episode, when there was the balance of payments crisis, but we tried to deal with it through this foreign exchange budgeting. That clearly put a break to the exchange rate. Once again, we come to the ’60s and the same issue remains. Remember that even if inflation is 5% a year, in 15 years, prices double at home. If your nominal exchange rate is fixed, then for a dollar’s worth of exports, if you are previously getting—our exchange rate was 4 rupees 76 paise—you’re still going to continue to get 4 rupees 76 paise for each dollar’s worth of exports.

The domestic prices have doubled. Your profitability domestically has doubled, so you sell at home. You see this import restriction automatically turns into an export restriction. In technical terms, of course, we would know this theorem which we call the Lerner’s Symmetry Theorem, which effectively, which says that, look, if you impose 10% across the board tariff on every product, that will have the effect which is exactly identical to a 10% export tax. Where this theorem comes from is the fact that when you impose this 10% across the board import tariff, you’re importing less. Then there is a need for exports to decline correspondingly. Correspondingly, your exports decline also.

RAJAGOPALAN: Basically, there are so many things which are entangled here, but all of it comes down to the principal point of the original problem of an autarkic regime. The moment you decide to close yourself up to trade, it becomes very difficult to pick and choose that these are the areas where we’ll participate and benefit from the gains of trade, and these are the areas where we won’t participate and we’ll protect ourselves from the problems of trade or competition or something like that. If you engage in one, you get the other. That seems to be the more universal principle.

No matter which country seems to have tried this highly restrictive autarkic regime, they kill their domestic economy exactly because of what you said. Some of this is because of import licensing restrictions. Some of it is because of the way the foreign exchange is pegged. Eventually the entire system has to make sense. Exports and domestic production seem to be the sacrifices that are made to keep the system intact.

PANAGARIYA: Yes. In our case, of course, it also got entangled by the domestic interventions because the government was trying to also achieve a particular mix of production, very focused into heavy industries which could not be competitive for sure. We just didn’t have the comparative advantage in those industries. Our cost of production domestically was much higher than what it was of the other producers abroad. We couldn’t compete there at the same time. Where we did have comparative advantages was for labor intensive products that then were forced to push into these cottage industries, very tiny units. We couldn’t compete there either. Interventions at multiple points and, at all points ultimately, inefficiencies arose.

Export Subsidies and Anti-Export Bias

RAJAGOPALAN: This may be a good point for you to tell us how a country can simultaneously have an anti-export bias, but also have export subsidies as a very large part of its policy program which benefits certain groups. Now, the two seem antithetical. It doesn’t seem reasonable, but in fact both of them, if I understand correctly from your work, are unintended consequences of the same restrictive import system and the autarkic system. How do both of these exist at the same time in a country like India in the ’50s and ’60s?

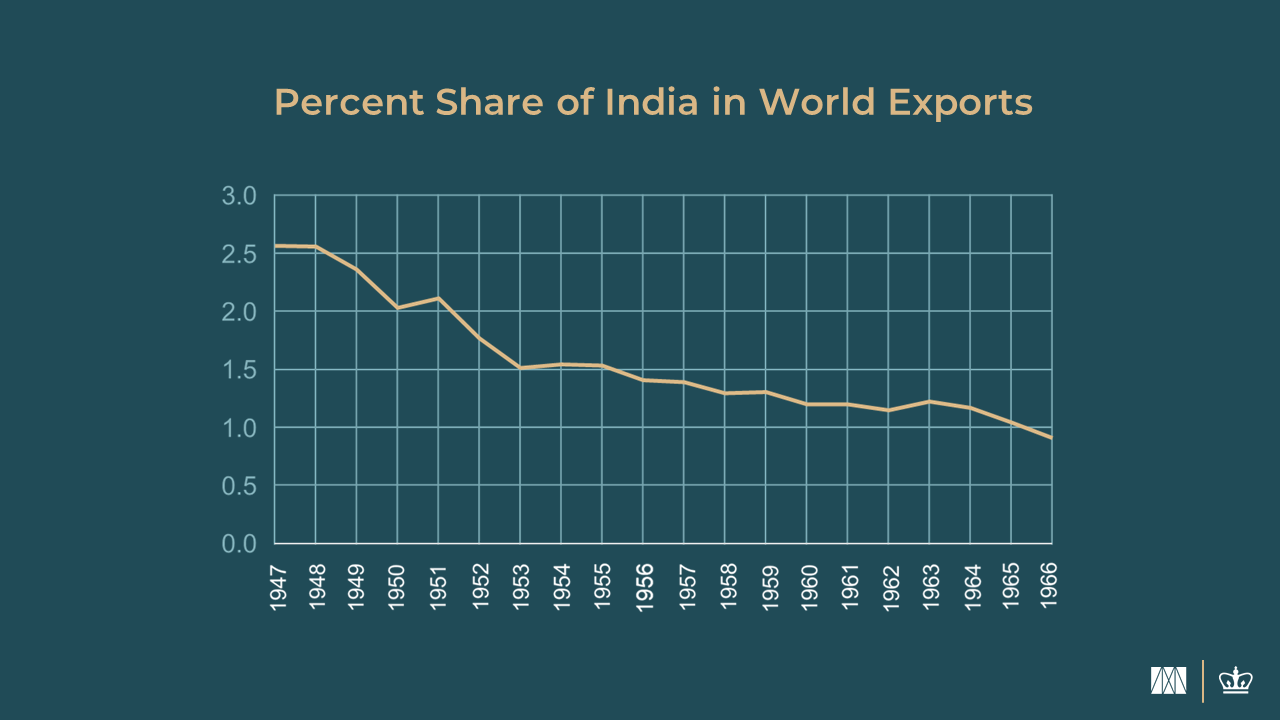

PANAGARIYA: I think this is a good point at which we can try to shift a little bit to look at the export policy as it was practiced during the ’50s and at least parts of ’60s. First and foremost, I think what we need to recognize is the fact that by now we know actually that the exports had suffered during these years. One measure of that is that India’s share in the global economy, which was a little above 2.5%—India’s exports as a proportion of the total world exports was a little more than 2.5% in about 1947. By 1966, it had dropped to below 1%, about 0.9%.

Clearly, relative to the global economy, we did very badly in terms of exports. That share never recovered for a very long time. Even after ’91, after we liberalized, even today our share in the merchandise exports is still about 1.7%. We are better than 0.9, but we haven’t gone back to the 2.5% still. Now, a large part of it of course happened because the exports in the global economy rose much more rapidly. During the years ’48 to 1960, the global exports were rising at 7% a year. India’s exports rose only 1.6% a year during that earlier period, so our share naturally declined.

That more or less continued into the ’60s as well. ’61 to ’66 global exports rose 8.2%. India’s rose only 3.4%. The share largely declined because—it’s not like in absolute terms India’s exports were declining, but they were declining relative to the global exports. By the way, that poor performance of exports evidently fed back into the import policy, because then you don’t have foreign exchange, you got fixed exchange rate. The only way you can then deal with your balance of payments is through restricting imports. That was the feedback that was happening.

Now on the export side, in the ’50s actually, we not only were indifferent toward exports. The attitude generally was one of indifference. If you look at all the debates that happened in 1955 around the second five-year plan, Mahalanobis model, all that, there’s basically an attitude of benign neglect. Nobody’s paying any attention. The assumption is that we are in an autarkic economy. That there’s no trade, even Mahalanobis model itself strictly assumes that the economy is completely closed.

Actually, in terms of policy, we did even worse because it was not pure benign neglect. It was actually one of abuse of export policy because we actually imposed restrictions, both physical restrictions on exports, and we used export taxes. Now here, there’s this book that everybody refers to by Dr. Manmohan Singh, our former prime minister, and also the finance minister from ’91 to ’96. He had written his Ph.D. thesis on India’s exports in 1962 at Oxford (sic), which later on came out in 1964 as a book. It’s a very nice analysis.

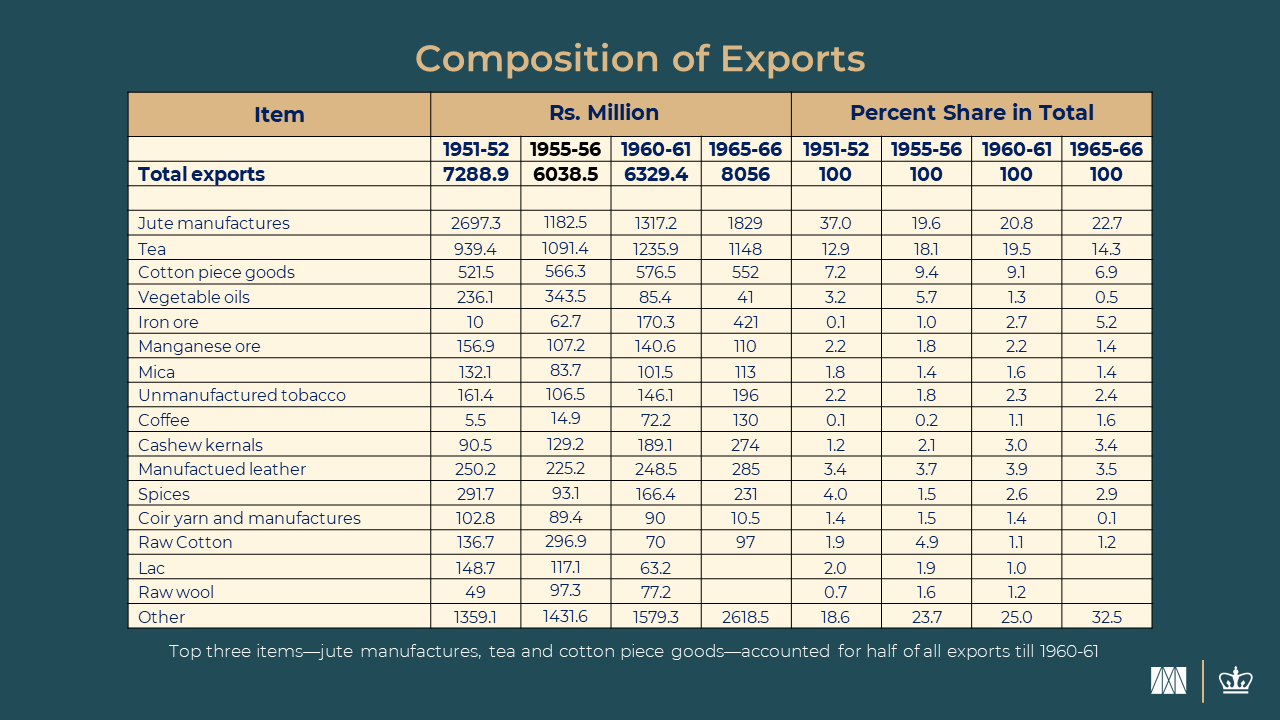

He doesn’t talk at all about the imports, he only focuses on the exports. The book title also reflects that—I have it here. Its title is “India’s Export Trends.” He only talks about exports, but documents that most of our exports were very traditional, things like jute manufactures, tea, cotton-piece goods, iron ore, manganese ore, largely very little of manufactures. Only cotton, that was our longstanding industry which had acquired some efficiency and so it had acquired export markets. But we were neglecting it at the time. But still because of its history it was surviving.

Now, what we did, however, during this period was also to use these export restrictions. Dr. Manmohan Singh really describes that even in the medium run, this is self-defeating. Because even when you have a very large share, what happens is that when you restrict, it opens the door to the competitors. Because obviously, when you restrict, you are using your market power to raise the price at which you can get for your exports. This is what a monopolist always does. That rise in the price also serves as an incentive to other competitors who were previously inefficient, but now they are able to compete, so they enter the market. Within a few years, they beat you.

Likewise, these export taxes have a kind of similar kind of impact. It’s the same thing; export taxes are also restricting exports. The importing countries, when they are faced with restrictions on exports by the exporting country, they begin to look for alternatives in both ways. They look for alternative suppliers for the same product, but they also begin looking for substitute products. Eventually, plastics, etc. came to replace the jute manufactures. A lot of the things for which jute was being used, then plastic bags came in, and they replaced it. There are these substitutes that come in.

There’s a very nice rendition of this in his book saying that these export restrictions are self-defeating, harmful. Because of this, by the early ’60s, we began to see that there’s a problem on the export side, exports are declining, something needs to be done. What do we do? Well, we go back and introduce export subsidies to some products. What we are trying to do is particularly things like chemicals and engineering goods. That is what we want to export.

Of course, with high enough subsidy, you can become an exporter of the products to some degree. Engineering goods did begin to emerge as export items. Actually, if you look at the full composition of exports, even till, as late as 1965, ’66, your traditional exports, top three, jute manufactures was your top export, tea was next and then cotton-piece goods—these are clothing, etc. Probably, they also include the fabrics. In the Indian classification, in the past we used to place both clothing and other textiles into the one category.

If you take those three, they accounted for more than 50% of the exports till at least ’60, ’61. Even as you get to ’65, ’66, when the engineering goods have begun to emerge, you have almost over 40% of exports are accounted for by these three, the traditional ones. Export subsidies, in the end, could only do so much.

The Bhagwati and Desai book gives you the estimate of what these subsidies were as a proportion of the price of the product. In some cases, these subsidies really rise well above 50%, which is not surprising given the fact that the nominal exchange rate was fixed and therefore, the real exchange rate was overvalued. What happened over this time, in the world market, is we lost share. Even in value terms—because in things like jute and tea, you’re trying to get market power—if market power is effective, at least in value terms, your export share should be rising, but it actually fell. In jute, we went from something like 86% in 1951 to 73% by 1960. In tea, we had almost 49%, around ’48 to ’50, fell to 43% ’58 to ’60. These shares actually even where we were so large, began to shrink. On cotton textiles, also we lost the market.

Share in Global Trade

RAJAGOPALAN: Something interesting is also going on in the rest of the world. One is, of course, you talk about our shares are declining as a share of global trade. The size of global trade itself is increasing in the postwar years. Post war, the developed countries see, for maybe two-and-a-half to three decades, the longest, peacetime growth that has probably ever been seen in history. Those countries are growing. Now, a lot of the goods were diverted in terms of demand for war goods, and I can imagine jute being one of those. Between the two World Wars, and in the immediate postcolonial period, I can imagine a lot of packaging material, moving material being a requirement.

You see that after 1950, in the developed world, most of the trade starts shifting more and more toward demand for consumer goods, which is something India is simply not making, whether it is for its domestic consumers, or for people abroad. It is still very much going along as if there’s a colonial government extracting iron ore and manganese ore. You’re basically sending out raw materials or tea. It just hasn’t somehow adapted to where the new world is going and what people seem to want to spend their money on.

PANAGARIYA: Yes, this was foretold because the other development literature is telling you that primary products have these low income and price elasticities, that as incomes rise there, the demand will automatically shift toward manufactures, as with these consumer goods. Price elasticity is high on those products, but very low on these traditional primary products. Even if you try to export a lot—and this is where, the great Bhagwati’s famous paper on immiserizing growth comes in saying that—even if you raise productivity, even if you do investments and you try to export a lot more of these primary products, the price will drop so much.

We, by the way, also face it today. We, in agriculture, are continuously trying to raise the output. Where can you sell this agricultural output? Price elasticity is extremely low. By the end of the day, you can’t do a whole lot of good by raising the output of these food grains, etc. through MSP. You raise the output through MSP, but in the market, the price will drop. For those farmers who have to sell their produce in the market, they basically will be wiped out. What we were doing was trying to go into heavy industry where we could not succeed in the global marketplace.

Consumer goods manufactures with South Korea, Taiwan, Singapore are succeeding big time, Hong Kong, they’re all succeeding big time in the ’60s. We are not, because, those are not the products we are doing. Very much self-defeating. Now, this is all hindsight, we can go back and do the analysis. This preoccupation that we are going to be powerhouses of engineering goods and chemical products and so forth is so strong at the time that nobody’s thinking, actually, of the light manufactures in India.

Even when it comes to subsidies, it’s not the export subsidies, it’s not the clothing and the textiles that are getting the subsidy; it’s the engineering goods and chemical products, which are getting the subsidy, but with a very limited success. That, of course, eventually gets us into a problem. You would remember the balance of payments crisis that we had, finally, in the mid-’60s.

Balance of Payments Crisis in the Sixties

RAJAGOPALAN: The first balance of payments crisis we spoke about last time, this was going on in 1958, which led to this foreign exchange budgeting sort of system. Now, the crisis in the mid-’60s is a little bit different. First, can you just walk us through what led to this balance of payments crisis in the ’60s?

PANAGARIYA: Yes, certainly. Look, first of all, we might want to ask a question here: Could things have been different? As I mentioned, Dr. Manmohan Singh’s book really did recommend devaluation. There was a lot of concerns still, and to be fair in the academic literature, there was a lot of the elasticity pessimism, which was that if you have a lot of market power in products—which arguably was there in the Indian case in things like jute and tea etc.—then your terms of trade in those products will really get worse.

That when you devalue, say, exchange rate goes from five rupees to eight rupees per dollar, that’ll create an incentive for these exporters to export more, and that will simply, because the low demand elasticity, depress the prices. He said that in whatever commodities you have that problem, put a modest export tax, but otherwise you devalue, and you don’t need to do any subsidies. That was his recommendation. Largely this kind of thing did happen later in 1966. We will come to that. A good question at this point is that, suppose this devaluation had been done earlier or something, could things have been very different?

My conclusion here is that some difference we could have made, and I’ve said before that 1958 was a good time, at that time we could have changed. Unless we were willing to change the industrial structure itself, unless we were willing to go back to doing consumer goods industries, light manufactures and move away from this heavy industry approach, in the end, we couldn’t have succeeded. The failure, as we will discuss in 1966, to some degree, was related to the fact that ultimately, we were not willing to change the industry structure.

If industry structure remains, that you’re trying to go into products in which you don’t have a comparative advantage, then the fundamental problem really remains. Your production structure is out of whack with your factor endowment, you are a very labor-abundant country but you’re trying to do highly capital-intensive industries. That always creates a tension. In a big way, we couldn’t have solved the problem, and as you can see, we are still struggling with that problem after 30 years of reforms. We are still struggling with that problem.

RAJAGOPALAN: That seems to me not just a problem of import policy or export policy or industrial policy as specifics. That to me seems a problem of the government simply cannot have such a large imprint on the economic system because it won’t be able to calculate effectively and mimic what the market would do in terms of sending resources to their highest productive use. The problem is even more fundamental. What you’re saying is there no simple fix and it has to fix the way it looks at industry.

I would take two steps back and say it has to relook entirely at the way it thinks about the economy and the way it thinks about people, and whether a mixed economic system under socialist planning with the Planning Commission is actually the correct way to go, or they just need to abandon that wholesale.

PANAGARIYA: This is all connected. If you are willing to accept that, look, my comparative advantage is in labor-intensive industries, then I should let the structure shift back toward those industries, then what you’re saying will follow. This is where Bhagwati and Desai’s 1970 book says that you did not need to have this licensing across the board on everything, and you did not need to have these import controls through licensing. Use tariffs, if you wish, on imports but otherwise let them come in. Use the exchange rate. If there are certain products which are absolutely desirable for the economy to produce, just do some better investment licensing on those products and leave the rest free.

If you really look at that book, it’s very much written during the political economy context of that time. They’re not saying that let the markets rip or something. It is not written at all in that kind of spirit. They see the political economy and so forth. What you are saying is roughly what the Bhagwati and Desai book says, that this intervention anywhere and everywhere is the problem. If there was a willingness to let the industry structure shift toward consumer goods, then what you are saying in terms of reduce interventions in the system would have followed.

Then you would not have needed to plan every single industry in that way. You’re precisely trying to produce things that the market will not tell you to produce, which forces then your hand to impose investment licensing.

RAJAGOPALAN: The systemic solution was not a possibility, that was simply not at the time being discussed as something to be done. Even within India, though there were specific suggestions like the one Dr. Manmohan Singh gave. Of course, in later years, Bhagwati and Desai come up with a much clearer, stronger critique of the system. At the time of, say, the early ’60s, other than devaluation, what were the possibilities? And second, what actually was the crisis that led to a point of devaluation that had to be done in ’66? What was going on then?

PANAGARIYA: By the ’60s, total dissatisfaction emerges from the industry because, you see, the ’50s was easier period. Number one, foreign exchange control was not there until ’58 at least. Licensing system, the bureaucracy could still deal with it because relatively few products, capital was limited anyway. And the signals went out that the chemical industry was what the government was trying to develop, heavy industries, steel, etc. Industrialists also know what to apply for in terms of the license. After this foreign exchange budgeting was adopted, then the system began to become complex.

By the ’60s, it was ’63 and ’64, you begin to see a proliferation of these committees about licensing, what to do, because a big backlog comes in. Also, the economy has grown a little larger, more applications are coming. Some of these numbers are given in my book “India: The Emerging Giant,” that license applications rise in numbers and all. Bureaucracy is not able to deal with it at least expeditiously. Delays become endemic and that leads the government to appoint a number of committees. There was the Swaminathan Committee, there was Hazari Committee, there were four or five of these committees; the reports come in.

The tragedy, of course, is that none of those reports is saying do away with licensing or do away with a substantial part of licensing, put licensing in certain sectors, and leave the rest. They’re not saying that. They’re just focusing on how I can improve the processes so that the licenses can be issued more rapidly. These committees painstakingly even record all the delays that are happening. The Bhagwati and Desai book reports: how many of these, in what sector, or how much delay was happening and how much of it was happening where. It’s all documented now.

The point was that the system was not thinking in terms of giving up the basic structure, either in terms of production or in terms of the policy regime. They’re just not willing to give that up. The crisis kept growing. A number of things happened. First of all, the agricultural performance, which was at least flat from ’60, ’61 to ’63, ’64. These are the first four years of the 1960s. But there was then a bumper crop for one year, ’64, ’65, after which there was drought. There were two back-to-back big droughts, ’65/’66, ’66/’67.

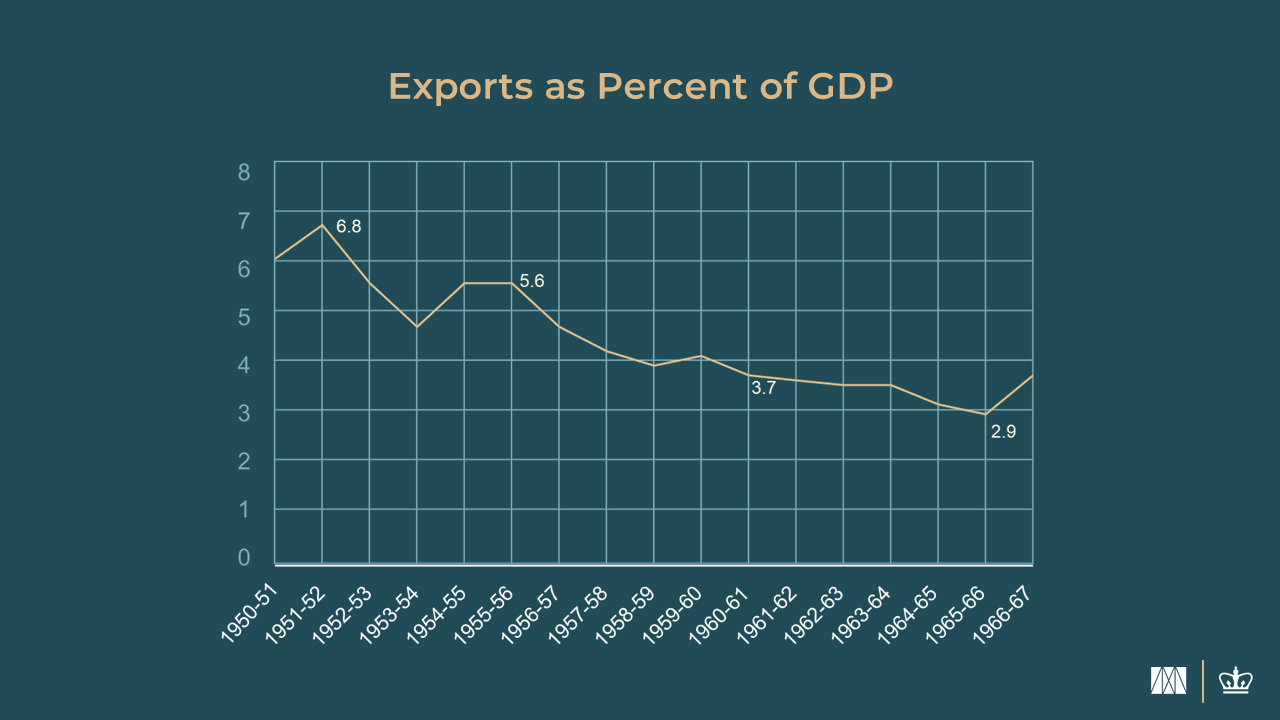

Those droughts actually play a very critical role, ’65/’66 drought particularly. Remember this ’65/’66 financial year is fully ending at the end of March 1966 and the devaluation happened in June 1966. This drought really played a very important role because, trade being so little, the industrial economy was also very tied into the agricultural economy. The drought automatically impacted the industrial economy also. Alongside this, the export performance was getting worse and worse in terms of the proportion of exports in GDP that was 3.7% in 1961, already low, it went to 2.9% by 1965, 1966. Your export revenues are declining badly, rising public expenditures were being financed by foreign borrowing and money creation.

You’re borrowing abroad, your debt servicing ratios are rising, a large part of the exports is being taken away by debt servicing—the interest in principle that you have to pay back—and exports themselves are declining. They then fall to 2.9% of the GDP by 1965/1966, so that puts the pressure on. Then partly, you’re doing money creation. Money creation is raising domestic prices. Again, domestic market is becoming more lucrative, so you want to stay away from exports, sell in the domestic market. Public investment was rising here as well. It rose 11.2% annually from 1961/1962 to 1965/1966. By 1965/1966, public fixed investment alone was close to 10% of the GDP, very large. The public sector was sucking up these resources and current expenditures of the government were rising.

China war happened, which led to the defense expenditures to rise. It’s unthinkable today to get to that level, but it used to be 2% of GDP in 1961. Became 4% by 1965/1966. Today, we are still not at 4%. We are well below. Consolidated fiscal deficit rose from 5.6% of GDP in 1960/1961 to 6.7% in 1965/1966. Loans abroad—even exclude your PL-480, that was like aid, even excluding that—the loans that you were taking, borrowing abroad increased from 1.4% of GDP in 1960/1961 to 2.4% in 1965/1966.

That service ratio, this is what I mentioned, exports as a proportion—sorry, the debt service interest in principle paid on foreign debt as a proportion of your total export earnings—were already 21% in 1966/1967. Now, one-fifth offset small export earnings are being taken away there. What do you do for imports? You’re clearly moving. This is exactly the thing that was happening, very similar in 1990, which led to 1991 balance of payments crisis. It was a very classic balance of payments crisis that you observe with fixed exchange rate systems, which don’t respond by devaluation and continue to domestically inflate the economy.

This is a perfect medicine, or you can call it poison, for the balance of payment crisis. This was being seen. And you remember all the episodes about India having to live the ship-to-mouth policy of Lyndon B. Johnson at that time. The U.S. is also getting impatient and has got some power because India is a big problem. It has to get the food grain from him. They were seeing that the crisis is growing. And the U.S. was also, by this time, realizing that heavy industry was the wrong thing to do. It wanted India to pay much greater attention to agriculture. It got the World Bank to come in here in September 1964. The Aid-India Consortium was very alarmed and they appointed this man called Bernard Bell.

RAJAGOPALAN: The Bell Mission.

PANAGARIYA: The Bell Mission. They came from the World Bank. They studied the situation. As asked, they made policy recommendations. They went and said, look, you have to shift away from heavy industry to agriculture. Of course, a very integral part of their package was this devaluation of the rupee. They also said put an end to licensing of imports, of at least intermediate imports. They said you can keep the licensing on the capital goods and consumer goods but not intermediate inputs. That’s sensible because if you’ve got this capacity that is unutilized because you’re not allowing enough intermediate inputs to be imported, that’s a loss to the economy. In principle, it’s the correct recommendation.

Then, a part of the package was also a substantial non-project aid for maintenance imports. Now, a part of the failure also happened, by the way, because that aid actually never came. Vijay Joshi and Ian Little wrote a thick book in 1994 on India’s macro where they cover this crisis in great detail. It’s a very nice history actually of India’s macro economy up to about 1991. The reforms and post 1991, they pick up in the next book that they wrote together. That was a shorter book. That book, they said that according to their sources, the government of India was expecting about $900 million of non-project aid for maintenance imports for several years, but that never materialized.

That really infuriated the Indian government, and this is why they then also felt free to reverse some of the measures that they had initially taken at the recommendation of the Bell commission. The Bell commission also had said put an end to export subsidies and to import licensing on intermediate inputs, and then substantial devaluation.

RAJAGOPALAN: Absolutely. In our 1991 Project, my colleague Prakhar Misra has done a really detailed timeline of the 1966 devaluation. It’s almost like a mirror. The crisis is very similar to the one in 1991, what happened in 1966, but not with the same results. He has a lovely paper and the book that you’re talking about, the Vijay Joshi book, we featured it on our website and our newsletter and so on. We will put in a link and everyone can refer to it. I want to also go back to the political situation within India, including the liberal voices, technical voices of economists and so on.

When there was an attempt to devalue the rupee in 1966, most politicians, especially important members in the cabinet, they were actually against it. Of course, the staunchest opposer of this was T.T. Krishnamachari, but there were a lot of people who were against the move, and even staunch liberals like from the Swatantra Party were not particularly in favor. What were the conditions under which this devaluation was implemented, though it was not exactly supported by the politics of the day?

PANAGARIYA: There was no alternative. You could say there was a TINA factor at work because, at the end of the day, India was, at this time, very dependent on food imports from the United States. I think that was a very critical factor in the whole thing and the U.S. clearly wanted this shift to happen, both toward agriculture and toward a more liberal regime and movement away from this heavy industry. Now, by the way, the U.S. also had played a very similar role earlier in South Korea. South Korea also, when they wrote their first plan in the early 1960s, there was some proposals for a shift to heavy industry in South Korea.

It never happened, but the U.S. also was advising them against that. There was some bit of that earlier. Although, in fairness, as far as India was concerned, at that time, they were giving aid to India without saying that the heavy industry is not very good. They actually supported it at that time. It’s not the case that their opposition to heavy industry in India had been there before. This is much later.

Anyway, I think that politically, you’re absolutely right that there was no constituency whatsoever in favor of devaluation. Manmohan Singh, by that time, was within the system, so we don’t know what his view was. He has never said anything, at least to my knowledge. Although his book clearly was quite favorable, so I would imagine that at least internally he was voicing support for devaluation.

Politically, Sachin Chaudhary was brought in at the time and he did the devaluation because the T.T.K. wouldn’t go along with it. A lot of opposition was there. Now, again, to be fair, one must also acknowledge the fact that economists were not in favor either. It’s not that many economists were in any way supporting it. Jagdish Bhagwati certainly spoke positively and I think Mrs. Gandhi did consult him. And certainly, he was supportive.

The fact is that political support was simply not there. Economists were, at that time, very much into this elasticity pessimism, because the exports are so price inelastic, devaluation might end up hurting rather than helping. There’s a lot of that academic literature from that period, that when is devaluation effective? We learned all about these Marshall-Lerner conditions. That some of the import elasticity should be bigger than one for the devaluation to be effective, and we failed with our products that we were actually exporting which were not so price elastic and, therefore, will not get the balance of payments improvement.

To some degree, the economics was also helping the political class which was opposed to it. Above all, I think in India this was really seen as externally imposed on India, and that never goes well in India. Anything that is seen as externally imposed simply gets rejected by the public. This is why 1991 reform was sold very carefully as India’s only—

RAJAGOPALAN: A homegrown, yes.

PANAGARIYA: —homegrown, and that this was India’s decision. Even in the way it was handled with the IMF and the World Bank was that we would send from our side the letter that, this is our plan, this is what we plan to do. It’s as though this is what we plan to do ourselves. If it fits into yours, then you give us the assistance. It’s as if chronologically we are the ones taking the action rather than the IMF saying that, if you do this, then we will—.

1966 was very clear. The Bell Mission had come in, the report was given. The recommendation came clearly from outside.

RAJAGOPALAN: Also, credit where credit is due to Prime Minister Indira Gandhi. In a sea of opinion where almost everyone was against the move, she was the one who had to decide whether or not they’re going ahead with the devaluation, and she was in favor. I believe there was a meeting between professor Jagdish Bhagwati and Prime Minister Indira Gandhi, and also K.N. Raj was consulted. Apparently, professor Bhagwati gave details on not only must India devalue, but how much it should devalue. Are you privy to the details of this discussion at all?

PANAGARIYA: No, I don’t think the discussion was there. I doubt it. Discussion was more about you know she was asking, what do you think will happen? Do you think this will get the export response? That’s my recollection from conversations with Jagdish.

One of the things that he always says while telling this story is that Mrs. Gandhi had the habit of keeping her head down, asking questions and then doodling on her writing pad. My recollection generally is that she was trying to feel out what the impact will be, which was not easily predictable, frankly speaking. I will check.

RAJAGOPALAN: That must be such a nice thing to have to pop into the next office and ask professor Bhagwati exactly what happened in 1966, which is lovely. Again, when we look back at that story, it’s the usual suspects. It’s B.R. Shenoy and T.N. Srinivasan and Jagdish Bhagwati who’ve written extensively about this episode of devaluation before and after. Aside from that, you’re right. The general view of the economists is not in support. The general view of the politicians is not in support.

The Failed Attempt To Reform in the Sixties

It seems to be some compromise like a TINA factor which this whole devaluation is pushed through. Is this perhaps the reason that after the devaluation, the liberalization one would have expected never really happened in India in 1966? In 1991, after the two-step devaluation in early July, there were a series of trade reforms and industrial licensing reforms and so on that were announced. This was that opportunity for India in the mid-’60s, but it never quite worked out.

PANAGARIYA: There are multiple problems here why it could not have worked out. First and foremost, again, are we willing to let the industry structure be determined a lot more by the market forces? That was the most crucial thing. Without that, there was no play. You’ll run into the same problems going forward. Either you continuously keep tightening your import regime so that your balance of payments remains manageable. The other alternative is to actually let go of the investment licensing. Let the market decide what the people want. What are the products for which the actual demand exists. Without that, I don’t think you could have succeeded. You see, this is why I also think that 1991 reform trade liberalization could not have succeeded because we also gave up all the investment licensing at that time.

There were multiple steps taken which were essential. There was an extra problem actually in the mid-’60s, which is exchange rates. You have to be prepared to devalue more. Shenoy, as you know, actually has written that, in his view, the failure was because devaluation was too little; a much larger devaluation was needed. I think he’s right because, just think about it, the nominal exchange rate had been fixed since 1948 or 1949, somewhere there, at 4 rupees, 76 paise per dollar until 1966. You got practically almost 18-, 19-year period. If your prices have more than doubled during that period domestically, and similar inflation has not happened abroad, then you had to devalue by much larger volume. You have to go to something like at least 10, 11, 12 rupees to the dollar. We went to only 7.5 rupees to the dollar.

Broadly speaking, I agree with Shenoy’s analysis that the devaluation itself was too little, but then I think actually Bhagwati and Srinivasan also point out that in terms of the value of the rupee, devaluation meant that the value declined by 36.5%. That was the extent of devaluation, value of rupee, when you do the calculation going from 4.76 rupees to the dollar to 7.5 rupees to the dollar. That is a decline of 36.5% of a rupee’s value in terms of the dollar, but the actual devaluation was even less because many of the export subsidies were cut out and import tariffs or import premium got reduced. Both of those factors also contributed to the devaluation being less than this 36.5%.

Actually, Bhagwati and Desai, they give a calculation and they say that effective devaluation turned out to be only 17.5% for exports because previously, for each dollar’s worth of exports, you were getting some subsidies also, which got taken out. Now, for a dollar’s worth, you are actually getting 7.50 rupees instead of 4.76 rupees, but then on top of whatever export subsidy you were getting on 4.76 rupees, let’s say another 2 rupees, if that’s taken out, then on net, you’ve not got the difference between 7.5 rupees to 4.76 rupees paise. 2 rupees in between have also gone away. The extra is much less. That is their point. The actual devaluation for exports on average was only 17.8% instead of 36.5%, and for imports, it was 29.7% instead of 36.5%. Shenoy would say that you needed much more devaluation, much larger, but what you got actually was not even 36.5%. It was insufficient.

Then, the two back-to-back droughts further complicated this. Because June 1966, the devaluation happens, but the drought is continuing the entire year of 1966, 1967, which means till March of 1967, this drought is continuing, and so the prices are rising. Domestic prices are rising. Those rising domestic prices then further undermine the devaluation. Meaning the domestic goods are becoming more lucrative now, even within a year of this. You could say it was a death foretold, meaning that you could have expected that this is how it’ll turn out. At least, that’s how it looks in hindsight.

Trade Policy Post Devaluation

RAJAGOPALAN: In the immediate aftermath, the cash subsidies, the import replenishments, all of these were brought back, reducing the effective devaluation. How does this inform what is the trade policy that will follow? You’ve devalued. You’ve obviously not devalued sufficiently. Now, what is a good way to think about how the policymakers at that time were thinking about trade policy post devaluation without implementing any liberalization reforms?

PANAGARIYA: They begin to see the failure, which is that the exports have not responded. Now, it’s not failure per se actually. It’s failure because exports don’t do better, but that doesn’t mean devaluation failed because exports would have done even worse. That counterfactual nobody looks at. Nobody worries about the counterfactual. You only look at, here is what were the exports before, and here are what the exports are after and you say devaluation has failed. Of course, if we had not devalued, the crisis would’ve been even bigger. Devaluation didn’t quite fail, but it’s simply that it did not deliver the outcome that we needed and that was not because devaluation failed, but because devaluation was not large enough. This withdrawal of export subsidies and import tariffs further undermined the effectiveness of the devaluation.

That’s exactly what happened which, of course, meant that any support that the Bell Mission package had disappeared very quickly. Export subsidies did return, as you just mentioned, so we did not continue on the paths to liberalization because they said, well, what do we do? We’ve got to now do something else to get more exports, and so export subsidies do come back. By 1970/1971, the import controls were back in full swing and even more stringent then than they were prior to devaluation. This is the conclusion of Joshi and Little who say that import controls by 1970/1971 were far more stringent now than they were even before in terms of its implementation.

Bhagwati and Srinivasan say that the combined export subsidy as a result of these measures on some selected items, including engineering goods, chemical, plastics, and other new products—they gave these numbers—say that they’ll range something between 50% to 90% on the effective ad valorem basis. It’s very large. It was on selected items, of course. They were trying to subsidize. Elasticity pessimism always kept them more on the side of restraining the exports rather than stimulating, but on products like sports goods, paper products, processed foods, they try to give subsidies and these were between 50% to 90% of the effective ad valorem value of the products. That’s where we came back.

RAJAGOPALAN: Earlier you had talked about how until there was a shift in industrial policy at home, there’s only so much that all this devaluation and the external sector reforms can work out or succeed. What you see after 1967 is Mrs. Gandhi’s government is now doubling down on socialism at home in a whole new way. It’s doubling down on heavy industry. They’re talking about commanding heights of the Indian economy. They’re nationalizing general insurance. They’re nationalizing coal mines, copper mines. There is a big wave further cementing India’s heavy industry policy which is at play.

Simultaneously, because of all the union problems, there are hundreds of cotton textile mills which are now going broke and not allowed to exit. At that time, you have all these sick textile mills, legislation which is passed. These are all nationalized by the government. The mills become defunct. There is that problem going on simultaneously. And it seems like the Indian domestic economy is more restrictive than ever before, which means all your import restrictions and export restrictions can’t be that far behind when the situation at home has now doubled down even more on the bets that Nehru made.

PANAGARIYA: Yes. Now, as we move forward in time, one might ask a good question, that if it was around, say, 1970 or a little later, if a similar crisis were to happen not in 1966 but a little later, would Mrs. Gandhi have devalued? My guess is that she wouldn’t have. See, 1966, 1967, she is a very new prime minister. It’s January 1966, Lal Bahadur Shastri died in Tashkent, and she became the prime minister. At that time, she’s still a very weak prime minister, if you will. Her own position is not so secure, but then by 1970, of course, she is in an incredibly commanding position. Probably at that point, she would have dealt with Lyndon Johnson very differently.

RAJAGOPALAN: She would have dealt with Lyndon Johnson differently, but on the other hand, it’s a little bit strange when people become very dictatorial, then they may also make bolder moves. It’s very difficult to predict the counterfactual when you have people in full dictatorial mode and have consolidated all power within their party and they’re ruling their cabinet, there’s not too much opposition from their cabinet. I feel like with Mrs. Gandhi, it could have easily gone the other way also. I’m never able to predict.

PANAGARIYA: Yes. The reason I say that is that she was on a very heavy socialist binge. Everything she was doing was moving toward more and more control.

RAJAGOPALAN: And P.N. Haksar is right now her chief adviser. He really is following the Soviet Union playbook at this point.

PANAGARIYA: Exactly. This is why I think that is the direction she would have taken. The economy’s direction is very clear around this time and so clearly the consistent thing to do would be to then absolutely refuse to devalue, and just double down on the controls, which they did.

RAJAGOPALAN: FERA, MRTP, everything becomes more restrictive. All these are also being amended simultaneously as the controls get heavier and heavier. More of the areas of activity are getting criminalized. It’s becoming very difficult to do business internally and with players abroad if you’re an Indian businessman around that time. Then, of course, the Emergency happens, and that’s the wildcard event that no one predicts. I imagine that until mid-1975, as the restrictions get more and more severe, and then the Emergency, when the economy is almost in suspended play for a while, all major policy is not being thought out carefully.

Then we get to the late ’70s, and you’ve talked about how starting in the late ’70s up to 1991, there is definitely a period where India starts thinking about relaxing restrictions. Then, of course, post 1991, we have the really very bold reforms. I think this is a nice place to end now, and then the next time you can walk us through the late ’70s, early ’80s period of what’s happening in India. How are we thinking about relaxing these very severe restrictions? What is the impact that leads us up to the 1991 reforms?

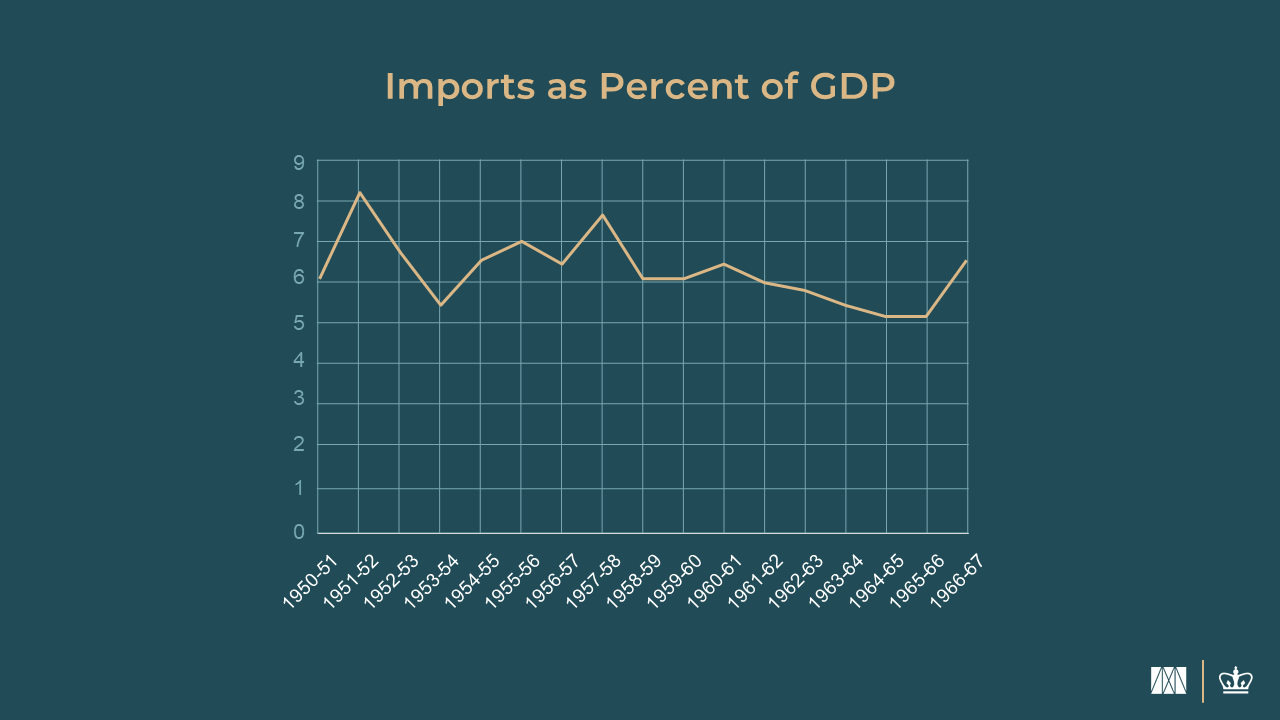

PANAGARIYA: I think so. Let me just say one final thing, that these controls, the very severe control regime that came to be had a major impact. One measure that we conventionally use is imports to GDP ratio. That really declined steadily. One way to think of it is that in the 1950s, imports never fell below 5.5% of the GDP. In fact, at peak in 1957, 1958, they were 9.3% of the GDP. Roughly, you can say between 5% and 10%. By 1969, 1970, imports, as a proportion of GDP had fallen to 4%, and a good part of it was probably also being spent at the time on food imports.

You can imagine how the industry had to function because there are so many raw materials, immediate imports, et cetera, that you need but nothing is happening. Even till almost mid-’70s, imports don’t rise even to 5%. It’s post mid-’70s that some expansion happens. That, of course, is what we can discuss in the next episode. What were the factors that led to some relaxation of the balance of payments constraint and so forth, which allowed for some bit of liberalization that happened beginning roughly in the mid-’70s?

RAJAGOPALAN: Mid-’70s. I think that’s a great plan, and I’m excited because as we get closer and closer to the liberalization episode, and also more recent in time, I think it starts becoming visible that everything happening in India today is so tightly linked to some of the measures that were taken in the ’80s and ’90s, so I’m really looking forward to that discussion. Thank you so much, Arvind. It’s always a pleasure.

PANAGARIYA: Likewise. Good. Thank you, Shruti.

View More